Property Portfolio Sequence: Four Stages, One Order

- Sam

- 2 hours ago

- 5 min read

Four stages define how serious property portfolios are built: primary residence, cash-flow asset, appreciation play, legacy hold. Most investors understand what each stage involves. Fewer understand that the order matters as much as the asset, and that building these positions out of sequence is the most common way a sound individual decision becomes a structural problem at the portfolio level.

The standard pattern in practice looks different. An investor finds a project they believe in and commits. A second position follows when capital is available. A primary residence sits somewhere in the mix, neither fully home nor fully investment, doing the accounting work of neither. The portfolio that results can contain genuinely good assets and still underperform, because the positions were never designed to support each other.

Property portfolios carry friction other asset classes do not. Acquisition costs run in the range of four to five percent before financing. Holding costs arrive monthly. Exit timelines are measured in months or years, not hours. Each position exerts force on the others. A cash-flow asset behind an appreciation play changes what that play can withstand. A primary residence that was over-capitalized restricts the available position size for what comes next. Sequence is not a preference. It is architecture.

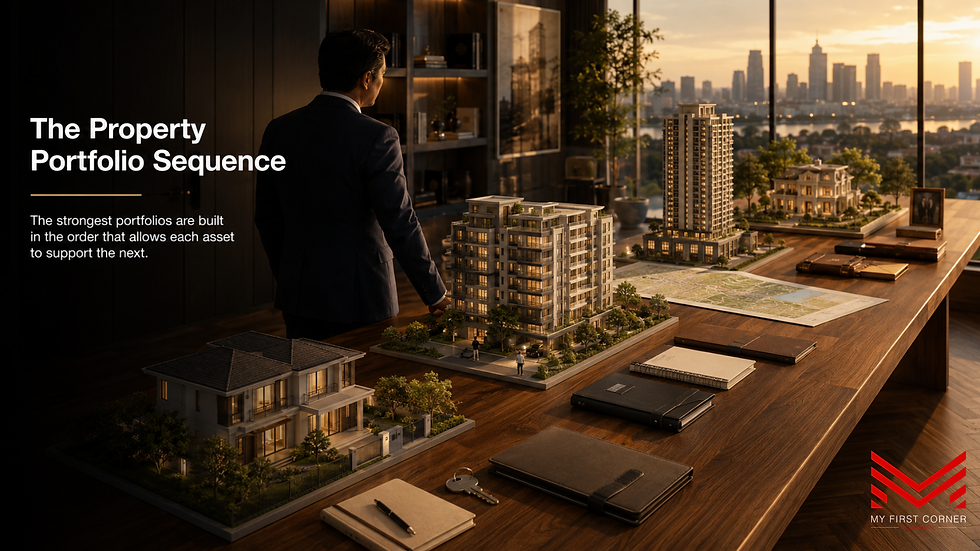

The property portfolio sequence

The framework is four stages, each with a distinct function: primary residence establishes cost control, the cash-flow asset builds recurring income, the appreciation play captures asymmetric upside, and the legacy hold is what the portfolio becomes when it no longer needs to be managed for survival. Each stage creates the conditions for the next. Reverse the order and the dependencies invert: the investor is now solving problems at stage four that were created at stage one.

The primary residence: cost control before capital deployment

The primary residence is not an investment in the yield sense of the word. It produces no income, generates no quarterly distribution, and contributes nothing to the cash-flow column. What it produces is a fixed cost of shelter that belongs to the holder rather than a landlord.

That shift is more consequential than it reads. A family paying rent carries a variable cost structure: the rent can increase, the lease can end, the housing cost is not controlled. A family holding a primary residence has converted that variable into a known, fixed equity position. The monthly payment services an asset. The cost structure of the household becomes predictable. That predictability is what allows calculated risk elsewhere in the portfolio.

The mistake investors make at this stage is treating the primary residence as the first profit center. They over-capitalize the purchase, stretch the financing, and reduce the capacity for what stage two requires. The primary residence should be sized to what the family genuinely needs and can carry without strain. Speculation belongs at stage three, not stage one.

The cash-flow asset: the base that makes the bet possible

The cash-flow asset is the portfolio's engine. It is acquired second because it cannot be acquired first without compounding the household's exposure. Before the primary residence is secured, the investor is managing two variable costs simultaneously: a housing expense that cannot be interrupted and an income stream from investment property that can be. The primary residence removes one of those variables before the other is introduced.

The cash-flow asset's function is mechanical. It produces net income that reduces the portfolio's dependency on earned income. Gross yield is the figure that appears in project marketing. Net yield, after tax, vacancy, management cost, and maintenance, is the figure that compounds. In a market like Phnom Penh, where gross yields on stabilized residential positions have historically run between six and eight percent and resident-rate withholding tax sits at 10 percent, the net position still outperforms comparable markets across the region. That differential is worth understanding not as a selling point but as a portfolio mechanic: income in a stable currency, from a low-cost-base market, allows recycling into subsequent positions faster than higher-cost markets permit.

The cash-flow asset is also the position that determines what the appreciation play can sustain.

The appreciation play: held from strength, not from necessity

An off-plan unit in a district ahead of infrastructure completion, a pre-sale position timed ahead of a major catalyst, a land-adjacent play ahead of rezoning: each is an asymmetric bet. The upside is real. The bet requires patience. And patience, in property, requires the structural ability to not need the capital back on a specific date.

Without a cash-flow asset behind it, the appreciation play must be carried entirely by earned income. If the timeline extends beyond projection, or if a disruption interrupts earned income, the investor faces exit under pressure. Sold under pressure, an appreciation play produces average returns at best. Held through the inflection point it was underwritten for, the same position produces the kind of return that restructures a portfolio.

The instruction is precise: acquire the appreciation play only once the cash-flow asset is performing. The income does not need to fully cover the appreciation play's carrying costs. It needs to cover enough of them that the position can be held through a delayed timeline without forcing a decision.

The legacy hold: end state of the property portfolio sequence

The legacy hold is not a fourth acquisition in the way the first three are acquisitions. It is what one of the earlier positions becomes over time: the primary residence outgrown and retained when the family moved, the cash-flow asset that appreciated beyond the income's original value proposition, the appreciation play that matured into a stabilized position generating yield of its own. The legacy hold is defined by one condition: the holder does not need to sell it.

That condition carries more practical weight than it appears to. Every asset held under compulsion carries an implicit concession to whoever is on the other side of the transaction. Every asset held from optionality commands its price, its timeline, and its terms. The legacy hold is the point at which all of the earlier sequencing decisions compound into something transferable rather than liquidatable.

Cambodia's ownership framework is directly relevant here. No estate or inheritance tax applies to property held in the country. The friction that converts a well-built holding into an administrative burden in other jurisdictions does not apply in the same form. That structural absence is worth factoring into the sequence from the point of acquisition, not only at the moment of transfer.

The portfolio that works is not the one with the best individual assets. It is the one where each position was acquired in the order that allowed the next to be built.

Investors who understand the sequence tend to hold longer at each stage, face fewer forced exits, and arrive at the legacy position with something worth transferring. The work done at stage one does not feel strategic in the moment. It usually defines what is possible at stage four.

At My First Corner, the sequencing conversation precedes every acquisition discussion. A client's next purchase cannot be analyzed correctly without understanding what the existing portfolio requires. That conversation is available when it is useful.

Comments